The Most Important Loan Term

Is a 12.5% interest loan better than a 7% loan?

Pop quiz: which of the following 2 loan options would you take?

Most people see the interest rate and are automatically repulsed by the 12.5% option, but let’s take a closer look…

At this stage in my career, I’ve navigated dozens of loans ranging from SBA to conventional to mezzanine to “private credit” (translation: most of these lessons were learned from experience).

Recently, we refinanced some loans in one business and got a new loan for an acquisition which had me thinking about several aspects around lending:

The impact on earnings and cash flow (the terms)

The perceived difficulty in obtaining a loan (the process)

The risks that usually get overlooked by a borrower (guilty here)

Let’s stick with #1 on this list for today…

Why do you need the money?

The reasons for getting a loan are wide-ranging:

Buy out a partner(s)

Buying property or real estate

Funding a period of high growth

Covering seasonally slow periods

An acquisition of an entire business

Capital investment (machinery, vehicle, equipment, etc.)

(Usually the worst reason to get a loan is to fund sustained operating losses, but that’s for another day.)

Loans are an incredible tool when it comes to creating value and building wealth, they call it “leverage” for a reason, as it amplifies both good and bad results. Borrowing money is one of the key pillars to economic growth. It makes the otherwise impossible, possible (how many of us have a few hundred thousand dollars lying around at a young age to buy a home as an example).

But, as Spider-Man once said: “with great power comes great responsibility”

So today I want to focus on one of the core tenets of financing to help you get the most out of that value-maximizing loan you seek…

When I talk to people about loans, they’re always focused exclusively on the interest rate: “a 5% rate? that’s so low, must be a good loan!”

But in my opinion, your interest rate is always a secondary factor… the real driving force for cash flow is the payback period, or what’s known as the “amortization period.”

What is amortization?

Amortization = the repayment timeline and schedule for your loan. It tells you how long you have to pay back the loan and it’s the determining factor for the principal portion of your monthly payment.

Simple example. You borrow $500,000.

At 7% interest over 5 years, your monthly payment = $9,900

At 7% interest over 20 years, your monthly payment = $3,900

The difference is entirely driven by the amortization period (5 vs. 20 years) and you’ll notice it has monthly cash “savings” of nearly $6,000.

That $6,000 per month is meaningful… for most small businesses, that could make or break a single month.

Loan terms

Here are some of the important pieces in your loan docs:

1. Amortization period — How long until the loan is paid off? This drives your monthly payment more than anything else. Most conventional loans have a 5-7 year amortization, an SBA loan is usually 10 years, and a commercial mortgage is anywhere from 20-30 years. The bank’s determination will depend on the asset being financed (collateral) and the business’s cash flow capacity (among other factors).

2. Loan term vs. amortization period — These are not the same thing! The term is when the loan actually matures while amortization determines your repayment schedule. Let’s say you borrow $1m with a 7-year amortization and a 3-year term… your monthly payment is based off 7-years while the loan matures in 3-years (meaning you’ll either need to refinance, renew, or make a balloon payment to cover the balance).

This is not inherently bad, but you want to know it’s coming.

3. Interest rate (fixed vs. variable) — A fixed rate is just that, fixed, for the duration of the loan. A variable rate floats (usually tied to prime or SOFR), so it can increase or decrease over time. When rates are rising, variable loans get expensive fast. When rates are falling, they get “cheaper.” Most small businesses are better served by the predictability of a fixed rate.

4. Other terms — Notable items to watch for include: prepayment penalties, personal guarantees, collateral, covenants, excess cash recapture, etc. (these are for another day).

What to do with this information?

Most entrepreneurs want the lowest interest rate possible, which is fine; but your rate doesn’t optimize for maximum cash flow durability. If given the choice, I’m taking “maximum amortization period” over “lower interest rate” every time.

Why?

I want the lowest monthly loan payment (principal & interest) possible. This is built-in downside protection for slower months, and I still have the option of paying more principal if my cash flow is strong.

Flexibility is an entrepreneur’s most coveted goal.

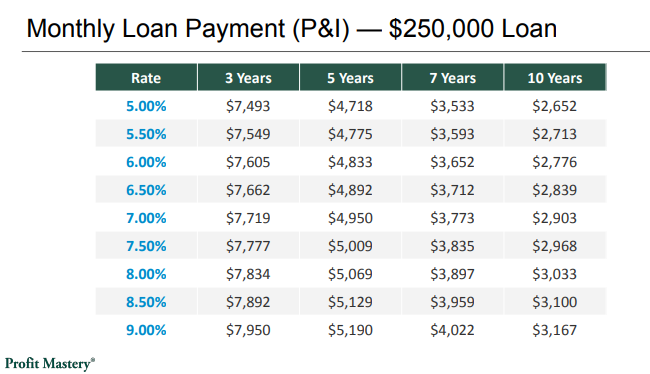

To see just how impactful this is… Here’s a table of a $250k loan with various interest rates and amortization periods.

Note the difference between a 10-year and 3-year amortization is >$4,000 per month while the difference between 5% and 9% is ~$400-500 per month.

Which are you optimizing for?

Can you afford it?

Look at your monthly payment and ask: does my business generate enough cash flow to comfortably cover this?

“Comfortably” means making that payment in both slow months and when things are good. That’s the key.

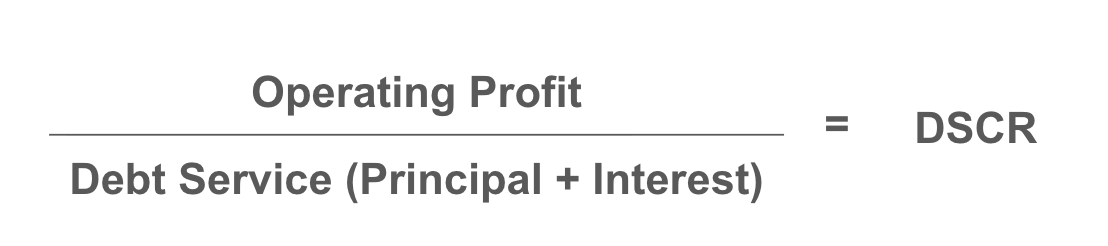

Banks literally measure this with the debt service coverage ratio (DSCR).

Take your annual operating profit (before interest and depreciation) and divide by your annual loan payment. A DSCR of 1.25x means you have $1.25 of operating profit for every $1.00 of loan payment.

Your bank wants at least 1.25x DSCR, but your goal should be higher than that. A higher ratio = more breathing room.

You should be calculating this DSCR ratio for a potential loan before you even set foot in the bank. This will guide how much borrowing is realistic for you and what terms you’ll need.

TL;DR

Loans are a tool for creating value (when used properly)

Interest rate and amortization period determine your monthly payment

Longer amortization period (years) = lower monthly payment

Lower monthly payment = maximum business flexibility for managing cash

DSCR measures your business’ ability to make your loan payments (track it)

And, as always, please read the whole thing before you sign :)

P.S. the “pop quiz” from the beginning? These loans have the same monthly payment (principal and interest). Sure, Loan A will pay more interest over the 25-year life. But it comes with $1.5m additional capital to deploy! The real answer depends on what the money is being used for.