EBITDA — Bullsh*t Earnings?

EBITD-ah!

Last week, at a well-known franchising convention, I saw a person wearing a hat with “EBITDA” stitched on it and had to have one of my own.

Charlie Munger famously called EBITDA “bullsh*t earnings” (I don’t completely agree with this). So it had me thinking about this measure of earnings and its relevance to you. Buckle in.

What is EBITDA?

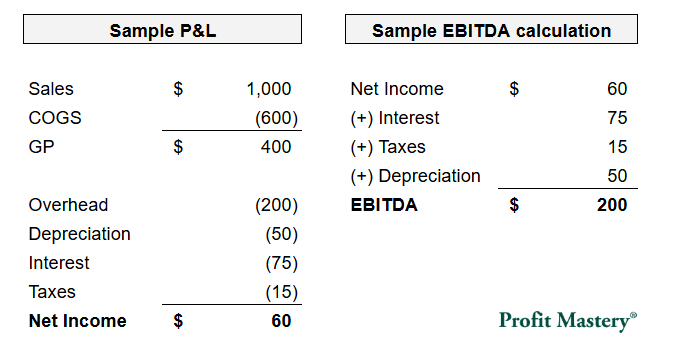

“Earnings before interest, taxes, depreciation, and amortization” is the formal definition.

It’s an earnings measure further up the P&L. If net income is the “bottom line,” then EBITDA is closer to the middle. Said another way, it’s your gross profit minus your overhead expenses.

Why exclude interest, taxes, and depreciation when they are very real costs? We’re excluding interest because different owners can choose their amount of borrowing, taxes because different owners have different tax rates, and depreciation because different owners can choose their level of capital investment.

Some of you might be thinking: “this isn’t relevant to me,” but hang on a moment...

Why it matters

This metric has several practical use cases:

Bankers use it as a measure of leverage

Buyers use it as a common valuation metric

Private equity uses it as a proxy for cash flow

Owners use it as a measure of “core business activity” earnings

Investors use it as a measure of “capital structure agnostic” earnings

Let’s break a few of these down.

Leverage — If EBITDA ignores taxes and interest, then technically it represents earnings available to both owners and lenders (i.e. it’s money available to pay both of these groups). Bankers want to see a low ratio of debt to EBITDA (plenty of earnings to cover outstanding debt balance) and a high ratio of EBITDA to interest expense (plenty of earnings to cover interest payments).

Valuation — Most buyers will want to look at your EBITDA. Many businesses are valued as a multiple of EBITDA (i.e. “4x EBITDA”). If your EBITDA is $500,000 and the industry average multiple is 4x, your business might be worth $2 million.

Cash flow — If someone came along and bought your company, they wouldn’t inherit your debt, or your tax rate, or your level of capital spending (depreciation). So EBITDA can reflect the earnings a new owner might reasonably expect out of your business. Hint: if you’re thinking of selling your company someday, this is a good metric to show prospective buyers!

Core business activity — If your business is profitable on an EBITDA basis but losing money after debt payments, that’s a sign you might have a financing issue rather than a weak business model.

Apples-to-apples comparisons — Let’s say you run a cleaning business, and you want to compare your performance to a competitor. If they financed their business with debt and you didn’t, their net income will be lower due to interest payments. But that doesn’t necessarily mean they’re less profitable. EBITDA lets you strip those factors out and compare businesses on a level playing field (i.e. capital structure agnostic).

So how could a small business practically use EBITDA?

For starters, you should organize your financial statements (chart of accounts) to keep items like depreciation, interest expense, and taxes below the EBITDA or operating income line (treat them as “other expenses” in QuickBooks parlance).

If you have any owner-dependent expenses, personal or otherwise, keep those below the EBITDA line item as well.

More importantly, if you want to stay one step ahead of your banker, this is a great way to track your leverage and risk metrics.

Takeaways — EBITDA isn’t perfect, but it certainly can be useful when used properly. It’s possible to have healthy EBITDA and negative profit which could mean too much debt.

P.S. — Where do businesses go wrong with this measure? 1) when they trick themselves into believing it’s actual cash flow (these are real expenses below the EBITDA line!); and 2) when they make aggressive add-back choices to “adjusted EBITDA.”

If you want to know more about EBITDA and using it in your business; reply with EBITDA to info@profitmastery.net.